A TU Delft student has found a way to keep the student loan interest as low as possible. Students who do this must suspend their loan and public transport card for a month.

Joep de Jong devised a way to save up to thousands of euros. (Photo: Justyna Botor)

On 1 January 2023, the interest on student loans is going up. Tertiary professional education and university students will be charged an interest of 0.46%. Vocational education students will be charged an even higher interest: 1.78%.

Higher education students who graduate with their diploma this year fall under the 0.46%. Later graduates will probably face a higher percentage. According to experts and student organisations, the interest will increase in the coming years. For example, a student who graduates in 2024 with a debt of EUR 45,000 can pay thousands of euros more in interest than someone graduating in 2022. A serious concern for everyone who cannot graduate this year.

Joep de Jong of TU Delft is just such a student. He currently has a debt of EUR 40,000 and still has to complete his internship and then graduate, which will take him nine more months. But he has found a way to profit from the lower rate. Joep discovered that it is possible to ‘fix’ the debt you have accumulated so far at the lower rate of 0.46%. All debt that accumulates after 2022 does fall under the future rate. “In other words, you split your debt,” explained Joep. The master student has had extensive contact over the past few weeks with DUO and approached Delta and other media organisations at the start of last month. “I wanted more students to be able to profit from this ‘trick’,” said Joep. Other students also discovered the existence of this DUO trick. Student Michiel Boeren posted about a similar trick on LinkedIn and NOS op 3 spoke with student Casper de Haes. The Dutch news organisation wrote an article about it and prepared this handy explanatory video (all links in Dutch).

Joep does add a warning message for his discovery. “You must be able to survive for a month without the student loan, a supplementary grant and public transport card by suspending them. Not everyone can afford to do that.” Before we look at Joep’s solution, let’s first explain how the student loan system and the interest percentage work.

When does DUO determine what interest percentage students have to pay?

Students who participate in the loan scheme and have graduated must pay back their loan after a grace period. They have 35 years to do so. The interest they pay in that period is fixed for five years.

Seems straightforward so far, doesn’t it? But watch out, because now it becomes more complex. The interest that you pay in the first five years is set in the year after you stop your student loan (for example, when you graduate and no longer collect the loan). To be more precise, that happens in the so-called ‘start-up phase’, the period of two years after graduating when you do not have to pay back anything yet. Higher education students who graduate in 2022 do not fall under the rate of 2022 (0%), but under the interest percentage that comes into force on 1 January 2023 (0.46%). The interest rate van 1 January 2024 applies to anyone graduating in 2023. The interest rate of 2025 applies to anyone graduating in 2024, etc.

How does DUO determine the interest percentage and how can students know it is going to change?

The interest percentage for the loan scheme of higher education students depends on the average interest at which the Dutch government borrows money for a period of five years. That is laid (in Dutch) down by law. Given the rising inflation, the interest rate is increasing, and given the situation on the financial markets, experts believe that the interest is unlikely to go down in the coming years. In other words: in 2024 the interest rate will probably exceed that in 2023.

Because the interest calculation is clearly laid down in law, it is possible to do the calculation yourself. The Financieele Dagblad newspaper did that earlier for 2023 (in Dutch). The interest rate in 2024 is not yet fixed officially, but experts and student organisations expect that it will be higher than 0.46%. That was the statement published by the Interstedelijk Studenten Overleg (Dutch National Student Association) in October in a press release: “This percentage will not immediately lead to serious financial problems. But we can imagine an ominous scenario if the interest keeps rising precipitously in the coming years.”

How can students split up their loan?

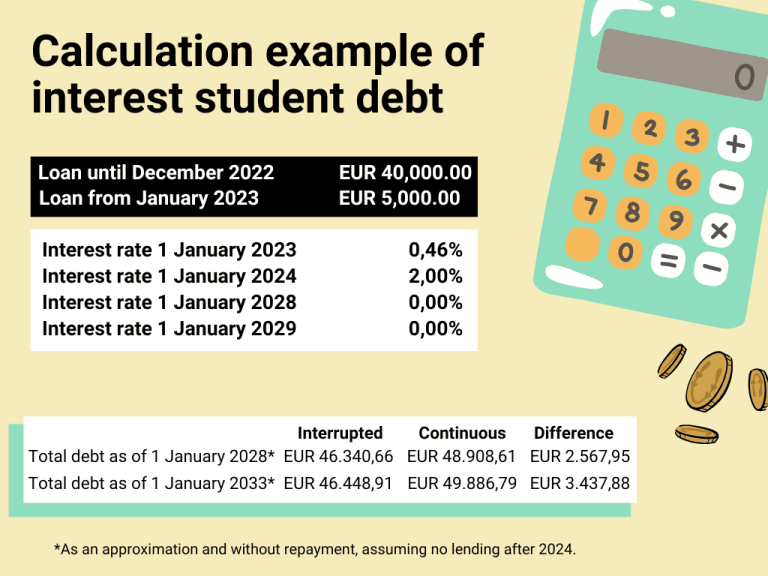

The short answer is: by not receiving study finance in January 2023 (consisting of loan, any supplementary grant and student travel product). If you do that and temporarily cancel your public transport card at the public transport ticket machine, the debt that has accumulated up to December 2022 still falls under the rate of 0.46%. From February, you can reactivate your loan, and start accumulating a new debt which will have a still unknown interest rate applied. Joep added, “Because this places part of your debt under a lower rate instead of your entire debt under a higher rate, you save money.” In Joep’s case it looks like the following.

Disclaimer: De rentepercentages van 2024 en de jaren daarna zijn nog niet bekend dus alle percentages na 2023 zijn fictief. (Visualisatie: Marjolein van der Veldt)

Disclaimer: De rentepercentages van 2024 en de jaren daarna zijn nog niet bekend dus alle percentages na 2023 zijn fictief. (Visualisatie: Marjolein van der Veldt)

In the long answer, we can provide more explanation: DUO allows you to stop your student loan. For example, you could take a gap year between the bachelor and master degrees. Imagine if a student graduates from their bachelor programme in August 2019, takes a year off and begins on a master’s programme in September 2021. What DUO does is split the student loan into two parts. The part of the loan the student accumulated during the bachelor phase is called ‘loan one’. The interest rate that applies to that loan derives from the associated start-up phase: the level is determined on the next January 1 after the last month that the student drew on the loan. The amount that the student borrows during the master becomes ‘loan two’. As long as the student is studying in the master programme, this is a current, interest-bearing loan. After the end of the programme, the interest rate is set for a period of five years.

TU Delft student Joep discovered that the same principle can be applied in a much shorter time period. Every year, DUO examines in February which students received the full student financing in January, consisting of a loan, public transport card and any supplementary grant. Students who did not borrow in January are considered by DUO as having completely finished the student grant. In other words: students can split their loan into two parts by not borrowing in January. This is possible while still studying. From February they can start collecting the loan again.

Given the likely comments that this primarily benefits the ‘rich’ students, Joep has come up with a solution: borrow more in December and buy a weekend free-travel product from the NS train service in January for EUR 31.60. “Borrowing more money is of course associated with costs and an NS-subscription does not always cover all your travel needs. Nevertheless, it can be more beneficial – depending on the amount of the student loan – than continuing to borrow,” said Joep.

Exceptions

There are also instances in which Joep’s solution does not turn out to save money. This is especially the case when the debt is low, for example, EUR 10,000. And more importantly: there are risks associated with splitting up the debt. It is possible that the interest will not follow the experts’ expectations and the interest may be less than 0.46% in the coming years. This would mean that the 0.46% is ultimately higher than the future percentage.

There are also a number of aspects that students must pay attention to. DUO spokesperson Tea Jonkman pointed out that students will have to ensure that they physically cancel their public transport card in time at a public transport ticket machine. “Otherwise you will still be registered at DUO as a recipient of a student grant,” said she. “In January you cannot use your student public transport ticket. The additional costs you incur as a result must outweigh the sum that you are saving.” She also warned that students around 30 years old must pay careful attention. “After your thirtieth birthday, you may not request a new study grant. In some cases it can thus be better to keep the loan current.”

OK, just to be clear: what does a student have to do?

- The most important point is not to blindly follow the tips in this article. Find someone who can discuss your situation with you, for example, a financial advisor or one of your parents/carers.

- Examine with them your current debt, your expected debt and the interest percentages you could expect in the future. You could ultimately prepare a calculation just like Joep.

- Only take a decision once you have calculated all the aspects.

- Would you like to split up your loan? Then you have to stop your loan, any supplementary grant and your public transport card for one month (January). You stop the loan in the online environment of DUO by clicking on the bright green button ‘stopping the student grant’. To cancel your public transport card, you need to go to a NS machine. According to a DUO-employee, this has to be done before January 10 at the latest. “But it is more sensible to do it on December 31,” added the employee. Because you may no longer use it to travel from the first day of the month.

- Ensure that you inform DUO in time – which is before mid-January according to a spokesperson – that you want to resume your loan, so you can receive funds again in February.

TU Delft student Joep prepared a model calculation that gives you an indication of how much interest you will save. That model can be found here (you can adjust the sums yourself after downloading the file). In his calculation, he assumed that the student has stopped borrowing in 2024 and that the student has not paid back the loan. In addition, the monthly interest on the loaned sum starting in 2023 has not been included. Joep stated, “The loaned sum increases by the month, which is too complicated for this calculation. You would need to know the loaned sum for each month.”

Text: Annebelle de Bruijn. Images: Marjolein van der Veldt. Special thanks to NRC editor Koen Marée.

Do you have a question or comment about this article?

[email protected]

Comments are closed.